Data Center investment India Vs Warehousing: New Real Estate Realty

The definitive expert analysis on investing in Data Centers vs. Warehousing in India. Explore key drivers (AI, E-commerce, 5G), risk profiles, and projected returns in this new commercial real estate battleground.

The bedrock of India’s economic narrative is transforming. For decades, the commercial real estate story was simple: office spaces and retail dominated. Today, two specialized, high-octane asset classes—Data Centers (DCs) and Grade-A Warehousing—have usurped the spotlight, triggering what is now the most compelling investment debate in the Indian realty sector. This is not a battle of growth versus stagnation; it is a high-stakes contest between two colossal infrastructure segments, each representing a critical facet of a digitized and globalized India. The stakes are immense, with investment projections in the DC space alone set to exceed $100 billion by 2027, while the logistics sector sails toward a robust $545 billion market size by 2030.

For institutional investors, private equity (PE) firms, and even High-Net-Worth Individuals (HNIs), the question is no longer if to invest in these emerging asset classes, but where to allocate capital for optimal, risk-adjusted returns. This analysis provides an expert-level dissection of the core drivers, operational complexities, risk profiles, and projected investment returns for both Investing in Data Centers vs. Warehousing in India, offering a roadmap to navigate this dynamic commercial realty battleground.

💾 Data Centers: The Hyperscale Engine of India’s Digital Ambition

The Data Center market in India is experiencing a hyper-growth phase, fueled by non-negotiable macroeconomic and regulatory tailwinds. DCs are no longer mere real estate; they are specialized, mission-critical utilities that form the physical layer of the digital economy. Understanding this asset class requires a shift in perspective from traditional square footage to megawatt (MW) capacity.

Key Growth Drivers Propelling Data Center Investment in India

The exponential growth trajectory of Investing in Data Centers in India is fundamentally driven by four non-linear forces:

The AI and Cloud Tsunami: Hyperscale's like Google, Microsoft, and Amazon Web Services (AWS) are investing billions of dollars to build massive AI infrastructure hubs. Generative AI and High-Performance Computing (HPC) workloads demand unprecedented computational power, requiring massive, GPU-dense data centers—a segment that offers significantly higher yields than traditional colocation.

Data Sovereignty and Localization Mandates: Government initiatives, including the Digital Personal Data Protection Act (DPDP Act, 2023) and the Reserve Bank of India’s (RBI) requirement for payment data to be stored domestically, have created a non-discretionary need for local storage capacity. This regulatory push guarantees a sustained, long-term demand curve.

5G Rollout and Edge Computing: The nationwide deployment of 5G is dramatically increasing data traffic and lowering latency requirements. This necessitates a shift from centralized, core DCs to distributed Edge Data Centers in Tier-2 and Tier-3 cities, opening up new geographic investment corridors beyond the saturated Mumbai and Chennai markets.

Digital Adoption in BFSI and E-commerce: The banking, financial services, and insurance (BFSI) sectors are undergoing massive digital transformation, along with the continued surge in e-commerce and OTT media consumption. This collective demand ensures high utilization rates for new DC capacity.

Investment Profile and Returns: A High-CapEx, High-Yield Model

Investing in Data Centers in India is characterized by a high barrier to entry but offers potentially superior, bond-like returns.

Capital Expenditure (CapEx) and Land: DC development is profoundly CapEx-intensive, costing between $7 million and $20 million per facility, largely due to specialized equipment (servers, cooling) and power infrastructure. Land suitability is the single greatest hurdle, demanding large, litigation-free parcels with immediate access to reliable, high-voltage power substations and fiber connectivity.

Revenue Model: The income stream is highly stable, often underpinned by medium-to-long-term, triple-net leases (10–20 years) with hyperscale tenants. Rents are calculated per kilowatt (KW) of power consumed, not just per square foot.

Projected Yields: Historically, data centers have commanded higher cap rates (capitalization rates) than most traditional real estate assets due to their mission-critical nature and higher operating risk. Yields typically range in the high single digits (7.5%–9.5%), significantly higher than prime Grade-A office space, compensating for the technological obsolescence risk.

🏭 Grade-A Warehousing: The Backbone of Consumption and Logistics

The warehousing and logistics sector is the physical manifestation of India's robust consumption story, dramatically reshaped by the Goods and Services Tax (GST) and the rapid maturation of the e-commerce supply chain. Investing in Warehousing in India has transitioned from a fragmented, unorganized business to a sophisticated, institutional-grade asset class.

Key Drivers Fueling Warehousing and Logistics Growth

The demand for high-quality, modern logistics space is driven by structural policy shifts and consumer behavior:

The GST Effect and Consolidation: The introduction of GST effectively broke down state borders, leading companies to consolidate inefficient, small legacy warehouses into large, strategically located Grade-A logistics parks (300,000+ sq. ft.). This consolidation continues to drive demand for modern, compliant facilities.

E-commerce and Last-Mile Sophistication: E-commerce penetration, particularly into Tier-2 and Tier-3 cities, demands proximity to the end consumer. This has spurred demand for both large regional distribution centers and smaller, urban-edge in-city warehousing for faster last-mile delivery, creating a diversified demand base.

The 'China Plus One' Strategy and PLI: Global supply chain diversification, coupled with the Indian government's Production Linked Incentive (PLI) schemes, is fueling a manufacturing boom. Automotive, electronics, and pharmaceutical industries require Grade-A, high-tech warehouses for raw material storage, assembly, and finished goods distribution, making Investing in Warehousing in India a strong indirect play on manufacturing.

The 3PL and Organized Retail Surge: Third-Party Logistics (3PL) providers now account for a substantial share of Grade-A space absorption, driven by the need to manage complex supply chains for FMCG (Fast-Moving Consumer Goods) and organized retail, which are rapidly expanding their SKU counts and geographical reach.

Investment Profile and Returns: A Lower-Risk, Scale-Driven Model

The investment thesis for Investing in Warehousing in India is attractive due to its lower technical risk and robust leasing velocity.

Operational Simplicity and Scalability: While still CapEx-intensive, the complexity is significantly lower than a data center. Warehousing focuses on large floor plates, high ceiling heights, and accessibility (proximity to national highways, rail, and ports). The asset can be replicated and scaled more easily across multiple micro-markets.

Revenue Model: Income is generated through traditional long-term leases (5–15 years) with fixed escalations, providing a highly predictable and secure cash flow stream, often with global institutional tenants (e.g., Amazon, DHL, FedEx).

Projected Yields: Grade-A warehousing yields are generally lower than DCs but are considered safer due to lower technological obsolescence risk. Core asset yields typically range from 6.5%–8.0%, with strong capital appreciation potential due to the continuous demand for Grade-A compliant space. The sector's stability has made it a favorite for global PE funds and India's first generation of real estate investment trusts (REITs) focused on industrial assets.

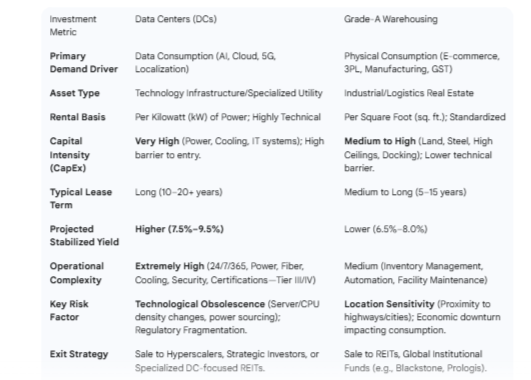

⚖️ A Head-to-Head Comparison: Data Centers vs. Warehousing

This is the core of the commercial realty battle—comparing the two asset classes across critical investment metrics.

Unpacking the Risk-Reward Spectrum

The decision of Investing in Data Centers vs. Warehousing in India hinges on a personal or institutional risk appetite:

Risk-Seeking Investors (DC): The higher yield of DCs is a reward for taking on specialized risks: the complexity of development, the enormous power dependency, and the long lead times for specialized equipment. An error in power planning or fiber route security can derail an entire project. However, successful execution locks in a tenant for two decades, delivering superior returns linked to India's unavoidable digital destiny.

Risk-Averse/Core Investors (Warehousing): Warehousing offers a lower-beta, less volatile investment. The fundamental need to move and store goods remains constant. While yields are lower, the asset is more fungible, easier to finance, and benefits directly from national infrastructure projects like the Dedicated Freight Corridors (DFCs) and the National Logistics Policy (NLP).

🏙️ Geographic and Regulatory Nuances: Where the Battle is Fought

The choice between DCs and Warehousing also dictates very different location strategies and requires navigating distinct regulatory landscapes.

Data Center Hotspots: The Power and Connectivity Core

The core DC battleground is fixed by access to two things: power and submarine cable landing stations.

Mumbai Metropolitan Region (MMR) & Chennai: These remain the undisputed champions, driven by their deep-sea fiber connectivity and historic infrastructure. Mumbai accounts for over 50% of the new DC supply pipeline, demanding massive land parcels in satellite areas like Navi Mumbai. Chennai, often called the 'Gateway to the East,' benefits from multiple cable landings.

Delhi NCR (Noida) & Hyderabad/Bengaluru: These act as critical inland hubs. Noida is emerging strongly due to proactive state policies (Uttar Pradesh Data Center Policy), offering incentives like stamp duty waivers and reduced electricity tariffs. Bengaluru and Hyderabad cater to the massive captive IT/Tech demand.

The main regulatory challenge for DCs is fragmentation. While the central government has given DCs infrastructure status (easing long-term finance), state-level policies govern land, electricity tariffs, and stamp duty. Savvy investors must analyze state policies meticulously—a stamp duty waiver in one state can dramatically lower the effective CapEx compared to another.

Warehousing Hubs: The Last-Mile and Corridor Strategy

Warehousing demand is driven by a hub-and-spoke model, focusing on consumption centers and transit efficiency.

The Golden Quadrilateral (Mumbai-Delhi-Kolkata-Chennai): This corridor is the perennial winner. Key consumption clusters like NCR, MMR, Pune, Chennai, and Bengaluru account for the bulk of Grade-A absorption.

Emerging Tier-2 Corridors: Cities like Lucknow, Jaipur, Coimbatore, and Nagpur are seeing unprecedented demand for regional distribution centers, driven by the expansion of e-commerce and 3PL networks seeking to cut down on delivery times.

The key regulatory advantage for warehousing comes from the National Logistics Policy (NLP) and the focus on reducing the total cost of logistics from 14% of GDP to 8%. The push for formalizing the sector and incentivizing multimodal connectivity makes the underlying investment safer and aligned with national economic goals.

🔮 The Operational Edge: Management and Mitigation of Risk

The long-term performance of Investing in Data Centers vs. Warehousing in India is ultimately determined by operational excellence and risk mitigation.

Data Center: Power, Precision, and People

The operational risk in a DC is existential. Failure is not an inconvenience; it's a catastrophic outage.

Power and Sustainability: The shift to Green Data Centers is an escalating operational mandate. The reliance on massive diesel generators for backup is quickly becoming fiscally and environmentally unviable. Investors must ensure the DC design includes options for direct PPAs from renewable energy sources (solar, wind) or relies on utilities capable of delivering five-nines (99.999%) uptime.

Talent Scarcity: Operating a Tier-IV DC requires highly specialized engineering talent—people who understand power electronics, cooling dynamics, and network security. Talent recruitment and retention in these niche areas are a growing operational cost and challenge.

Technology Refresh Cycles: While the building structure is long-term, the IT equipment (servers, racks) changes rapidly. Investors must factor in capital reserves for a technology refresh every 5–7 years to remain competitive, which is a key differentiator from traditional realty.

Warehousing: Automation, Efficiency, and Fluidity

Warehouse risk is primarily driven by market absorption and technological efficiency.

Automation Integration: The future of Grade-A warehousing is automation. Investors who build facilities with the specifications for Automated Storage and Retrieval Systems (AS/RS), high-bay racking, and robotics are future-proofing their assets. A 'smart' warehouse commands premium rents and attracts blue-chip 3PL tenants.

Land Banking and Clear Title: Given that land is 30%–40% of the project cost, clear land titles and proximity to infrastructure projects (ports, highways) are paramount. The ability to secure large, contiguous parcels is becoming a competitive moat.

Market Fluidity: Warehousing can adapt to changing tenants (e.g., from an FMCG to an e-commerce tenant) more easily than a highly customized DC. This greater market fluidity offers a better hedge against single-tenant risk.

Conclusion: Positioning Your Portfolio in India's Commercial Realty Battle

The battle between Data Centers and Warehousing is the most exciting development in Indian commercial real estate in decades. It represents a fundamental choice for investors: to bet on Information Velocity (DCs) or Physical Velocity (Warehousing).

The Strategic Data Center Investor is banking on India’s accelerating digital trajectory and the non-negotiable demand for in-country data storage driven by AI and regulation. They seek higher, utility-like yields and are willing to take on significant CapEx, operational complexity, and technological risk for a specialized, highly defensible asset class.

The Strategic Warehousing Investor is banking on the consistent, GDP-linked growth of India's consumption, manufacturing, and organized retail sectors. They value the lower-risk, highly scalable nature of the asset, which is shielded by macro-level policy support (GST, NLP) and offers robust, medium-to-high returns with a clearer path for institutional exit (REITs).

Ultimately, a balanced, expert-driven portfolio in the new Indian realty landscape should include exposure to both. The Data Center offers the high-growth alpha of the digital economy, while Grade-A Warehousing provides the indispensable beta of a rising consumption powerhouse. Understanding the distinct geographical, power, and regulatory dynamics of each is the key to mastering this new commercial realty battle.

Why Knowledge Park 5 can be Your Next Real Estate Investment?

Knowledge Park 5 is not merely an extension of the existing Knowledge Park philosophy; it is an evolution. It's designed to handle the next 20 years of Greater Noida's growth, accommodating larger, world-class institutions and a corporate presence that demands superior connectivity. Investors who enter the Knowledge Park 5 market now, before the full infrastructural benefits are realized, are positioned to capture the highest possible capital appreciation. The underlying fundamentals—educational hub demand, excellent expressway connectivity, and the Jewar Airport factor—solidify the investment thesis. It is the definitive 'buy-and-hold' location for superior ROI in Greater Noida. The time to invest in Knowledge Park 5 is during this phase of confirmed, but incomplete, infrastructure development.

Frequently asked questions

What is the primary difference in the investment profile when Investing in Data Centers vs. Warehousing in India?

The primary difference is the risk and capitalization structure. Data Centers are a high-CapEx, high-yield, technology-driven utility asset with long leases (10–20 years) and high technical obsolescence risk. Warehousing is a scalable, lower-CapEx, lower-risk industrial asset with medium-to-long leases (5–15 years), offering returns linked directly to the e-commerce and logistics growth story.

How is the investment in Indian Data Centers being driven by AI and data localization?

The explosion of AI and cloud adoption requires massive, high-power density Data Centers (hyperscale). Simultaneously, the Digital Personal Data Protection Act (DPDP Act) and RBI mandates require data to be stored domestically (localization). This dual pressure creates non-discretionary, guaranteed demand for new Data Center capacity, making it a highly attractive, long-term infrastructure investment.

Why is Grade-A Warehousing considered a lower-risk investment asset in India than Data Centers?

Grade-A Warehousing is considered lower risk because its demand is based on constant physical consumption, which is tied to GDP and population growth—a stable long-term trend. The asset is less susceptible to rapid technological obsolescence, the operational complexity is significantly lower, and the exit avenues (via REITs and institutional funds) are well-established.

What are the main challenges for a first-time investor Investing in Data Centers in India?

The main challenges are securing reliable, high-voltage power connectivity and managing complex regulatory approvals, which vary significantly by state. Data Centers have a high barrier to entry due to specialized CapEx, long equipment lead times, and the need for highly specialized engineering talent to ensure critical uptime.

How can I contact you?

You can reach us by 01169312815. We are always happy to answer your questions.

Can investment in the Indian warehousing sector benefit from the 'China Plus One' strategy?

Yes. The 'China Plus One' strategy encourages global companies to diversify their manufacturing and supply chains to countries like India. This directly translates into increased demand for Grade-A warehousing for storing raw materials, components, and finished goods, making the sector a strong indirect beneficiary of India's manufacturing revival and PLI schemes.

Knowledge Park 5

Knowledge Park 5 is rapidly evolving into a smart urban microcity , Strategically located in Greater Noida West. Knowledge Park 5 is a developing area with a focus on commercial and IT/ITES developments.

Connect

Growth